Panama has made significant strides in addressing its financial sector’s challenges, particularly in relation to anti-money laundering (AML) and countering the financing of terrorism (CFT). This report released by the International Monetary Fund (IMF) delves into Panama’s recent advancements, focusing on its exit from the FATF grey list, evolving corporate sector regulations, and recent developments in fintech and virtual assets. We will also explore the effectiveness of Panama’s financial intelligence unit (FIU) and its registry of ultimate beneficial ownership.

1. Panama’s Exit from the FATF Grey List and Corporate Sector Reforms

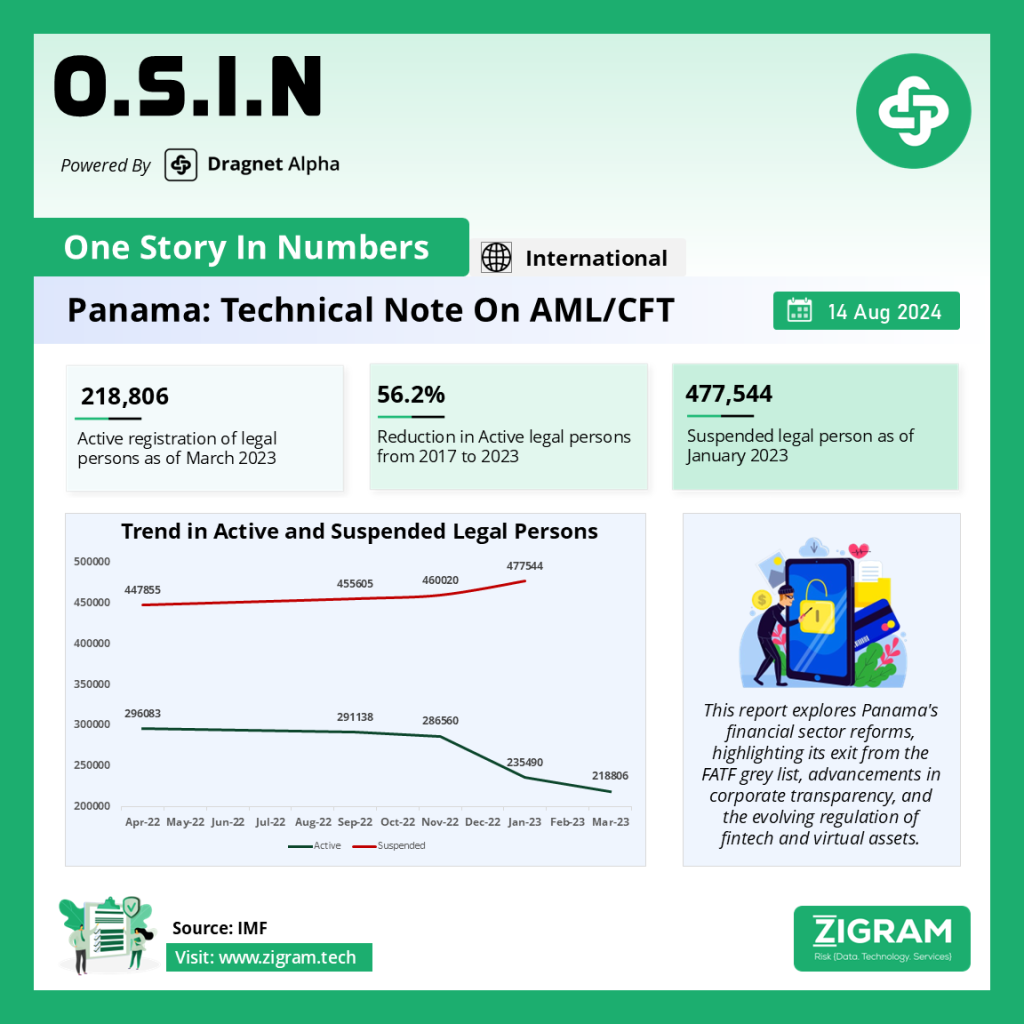

Panama’s exit from the FATF grey list marks a crucial milestone in its ongoing efforts to enhance its AML/CFT framework. The FATF’s Financial Sector Assessment Program (FSAP) report highlighted Panama’s progress in addressing strategic deficiencies and improving its financial regulatory environment.

A. Significant Progress and Recent Updates

Panama has undertaken substantial reforms to align its AML/CFT regime with international standards. Key developments include:

1. Strengthened Regulatory Framework: Reforms to Panama’s AML/CFT laws and regulations aim to address previously identified gaps. This includes enhanced supervision of financial institutions and improved compliance mechanisms.

2. Enhanced Corporate Transparency: Panama has made strides in increasing transparency within its corporate sector. This includes the implementation of more rigorous due diligence procedures and enhanced reporting requirements for legal entities.

B. Access to the Registry of Ultimate Beneficial Ownership (RUBF)

A pivotal aspect of Panama’s reform efforts is the establishment of the RUBF, designed to improve transparency regarding the ownership of legal entities.

1. Access and Usage: The RUBF is accessible primarily to competent authorities such as the SSNF, UAF, MP, and DGI. Only the SSNF has direct access to the RUBF, with designated officials responsible for providing information to other competent authorities upon request. Since November 2022, authorities have received training and access to the RUBF, facilitating domestic investigations and international cooperation.

2. Performance Metrics: As of May 2023, over 134 requests for RUBF information have been processed, with a 91% success rate. Competent authorities report satisfaction with the quality and completeness of information available in the RUBF.

3. Search Functionality: The current RUBF system allows searches only by the legal person’s name and folio number. Expanding search capabilities to include additional fields could enhance the utility of the RUBF for competent authorities.

4. International Best Practices: The FATF and other international guidelines suggest broadening search functionalities and considering public or partial access to beneficial ownership information to enhance transparency and oversight.

2. Fintech Sector and Virtual Assets in Panama

Panama’s financial technology (fintech) sector and virtual asset landscape are evolving rapidly, presenting both opportunities and challenges.

A. Financial Technologies

1. Operational Permits: Fintech institutions in Panama must obtain an operational notice from MICI. The process, regulated by Law No. 5 of November 2007, is automated through the “Panama Emprende” platform. However, the process currently does not require submitting beneficial ownership information.

2. AML/CFT Measures: The operational permit includes a general AML/CFT assessment. For regulated activities, additional reviews and approvals by sector-specific authorities like the SBP or SMV are required. Inconsistencies in determining which fintech institutions are subject to AML/CFT obligations could lead to regulatory gaps.

3. Regulatory Clarifications: Law No. 23 of 2015 lacks clarity in defining which fintech institutions fall under AML/CFT obligations. The narrow interpretation of terms related to payment means and electronic money may result in some fintech institutions being unregulated.

B. Virtual Assets/Virtual Asset Service Providers (VA/VASPs)

1. Current Situation: Limited digital asset transactions are reported, primarily involving foreign exchanges and enhanced due diligence by local financial institutions. Panama does not yet have a comprehensive legal framework for VA/VASPs.

2. Legislative Developments: Previous bills addressing VA/VASP activities were vetoed by the President due to concerns about regulatory adequacy and AML/CFT compliance. The latest bill is under consideration by the Supreme Court.

3. Future Directions: Authorities need to review and update AML/CFT measures to address risks from VAs/VASPs. This involves assessing emerging risks and developing a regulatory framework in line with FATF standards and broader legal reforms for payment services.

Panama’s ongoing reforms reflect a robust commitment to strengthening its financial sector’s integrity and aligning with international standards. While significant progress has been made, particularly in enhancing corporate transparency and addressing emerging risks in fintech and virtual assets, continued efforts are essential. Expanding search functionalities in the RUBF, clarifying fintech regulatory terms, and developing a comprehensive framework for virtual assets will be crucial in ensuring Panama’s financial system remains resilient and compliant with global best practices.

Read and Download the full report here.

Know more about the product: Dragnet Alpha

Click here to book a free demo.

- #DataBreach

- #Panama

- #FATF

- #FinancialReform

- #AML

- #Fintech

- #VirtualAssets

- #CorporateTransparency

- #Regulation

- #Compliance

- #Finance

- #IMF